Debt Consolidation Loans for Bad Credit Rates in December 2025

Bad credit? You have options. LendingTree users with bad credit get 7+ debt consolidation loan offers on average

Best debt consolidation for bad credit lenders with the lowest rates

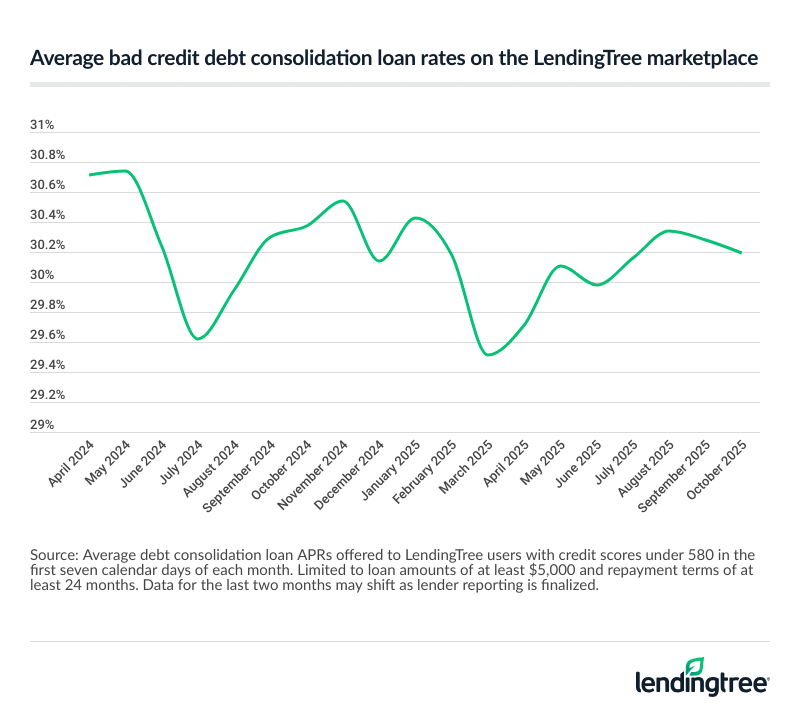

Bad credit debt consolidation loan rates averaging at 30.19%

Concerned about the high rate?

We have tips below to increase your approval odds and improve your credit score to lower your rate.

Debt consolidation loans for bad credit rate trends over time

Rates for borrowers with a credit score below 580 have remained under 31.00% for over a year. The average debt consolidation loan rate for bad credit on the LendingTree marketplace was 30.19% APR in October 2025.

What to know about debt consolidation loans for bad credit

It can be hard to know if a debt consolidation loan is right for you — or even if you’ll qualify for a loan that saves you money.

Debt consolidation loans help people like you combine multiple debts into one. The goal is to lower your monthly payments and the total amount of interest you pay.

If you have bad credit (FICO Score below 580), you might be wondering if you’ll even qualify. It’s possible, but you’ll need to compare the rates you’re currently paying with the ones in your offer to make sure consolidating is worth it.

Use the LendingTree debt consolidation calculator to see how much you could save with lower rates. When you get an offer, use our calculator again to see if you’ll save on the total cost of your loan.

Estimate how much you’ll save with your debt consolidation loan for bad credit rate

Why do millions of Americans trust LendingTree?

25+ years in business. 110+ million Americans served. $260+ billion in funded loans.

Security

Instead of sharing information with multiple lenders, fill out one simple, secure form in five minutes or less.

Savings

We’ll match you with up to five lenders from our network of 300+ lenders who will call to compete for your business.

Support

We provide ongoing support with free credit monitoring, budgeting insights and personalized recommendations to help you save.

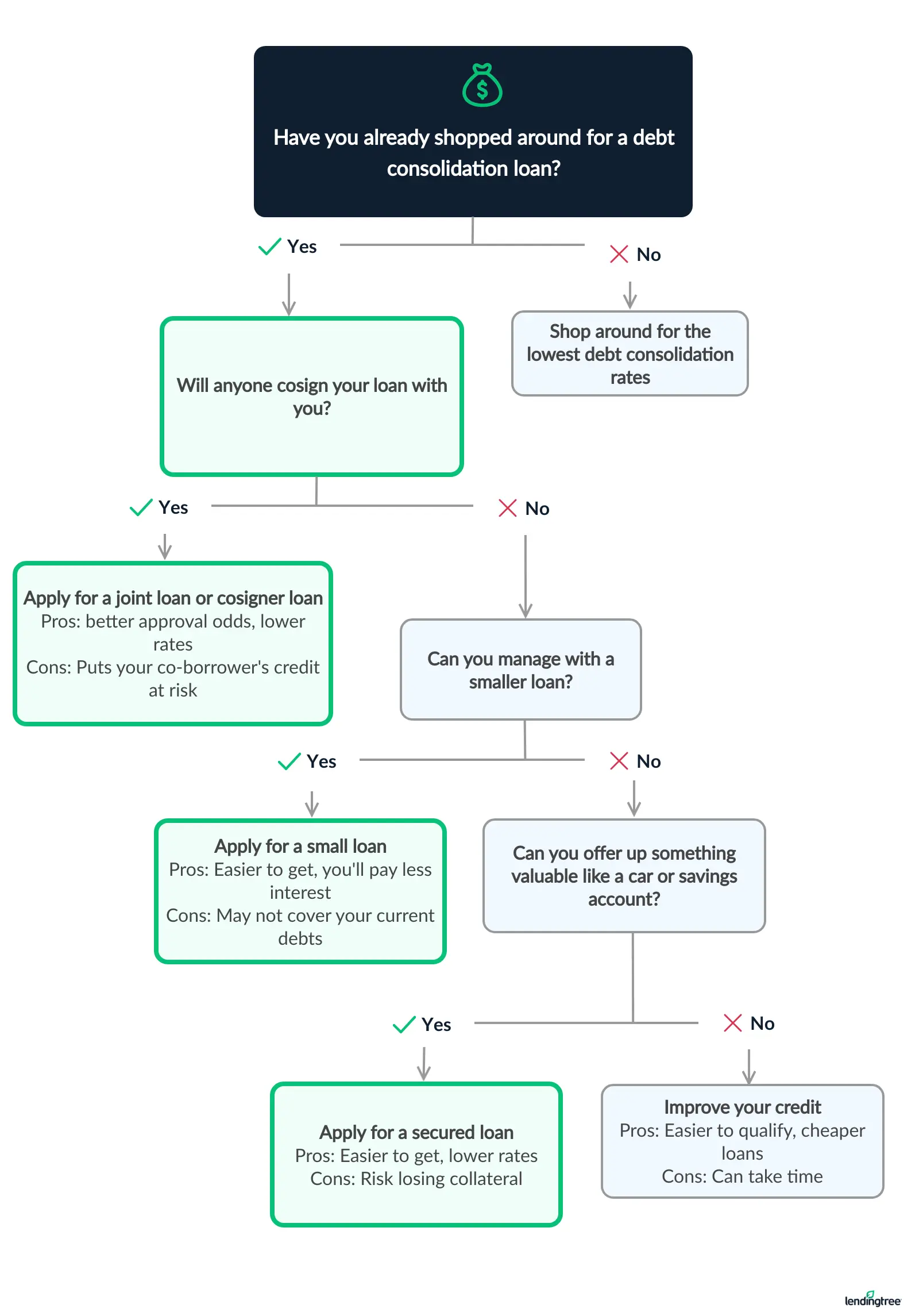

How to improve your odds of qualifying for a debt consolidation loan

Why use LendingTree?

$2.8B in funding

In 2024 alone, LendingTree helped find funding for over $2.8 billion in personal loans.

$1,659 in savings

LendingTree users save $1,659 on average just by shopping and comparing rates.

309,000 loans

In 2024, LendingTree helped find funding for over 309,000 personal loans.

What to do if you don’t qualify for a loan

Don’t qualify? You still have options. Consider the strategies below to help you manage your debt.

Debt management strategies

You can pay off your debt on your own with the right plan. Create a budget, limit your expenses and use extra money to pay off the debt. Consider different debt payoff techniques, and choose the one that works for you.

Improve your credit score

The best way to improve your chances of getting a new loan is to boost your credit score. Improving your score may take time, but using your credit responsibly can help bring your score back up. Start by making on-time payments and disputing possible errors.

Get your own credit report card for free with LendingTree Spring. We’ll show you how you’re doing on each of the factors that affect your credit, like payment history and credit utilization. Plus, we’ll give you personalized recommendations on how to improve your score.

Bankruptcy

Bankruptcy is a legal process that clears your debt under certain conditions, giving you a clean slate. The cons? You may have to give up some of your assets, and your credit will take a major hit. Bankruptcy can also affect your ability to borrow money in the future.

Debt settlement

Debt settlement services will likely hurt your credit score by encouraging you to miss payments and avoid contacting creditors while the company negotiates with them. There are risks to using these services, and you should consult a credit counselor before signing up.

Expert insights on debt consolidation loans for bad credit in 2025

Prioritize offers lower than your current rates and ideally below 36% APR, a common max for personal loans. Prequalify to get an idea of offers you could receive without touching your credit.

Should you get a debt consolidation loan if you have bad credit? If you can honestly answer “yes” to the following three questions, it’s likely a good financial move.

- Will you save money? If you have serious credit problems, you’ll likely have trouble qualifying for a good rate. Use our debt consolidation loan calculator to compare the interest rates on your current debts with your debt consolidation loan offers. (You can check your rates by prequalifying for a debt consolidation loan — it won’t affect your credit.)

- Do you have a plan to pay off the debt? Consolidation alone usually isn’t enough to help you become debt-free. But if you’re willing to follow a plan to get out of debt, a consolidation loan can be the first step in the right direction.

- Can you avoid new debt? Paying off your current debts with a consolidation loan and racking up more debt will land you in financial hot water. Make sure you’re committed to avoiding new debt, or consolidation could make your current finances even worse.

Having bad credit can make you an easy target for predatory lenders that offer payday loans or car title loans. These types of loans don’t typically require a credit check, but they come with high APRs and short repayment terms that can trap you in a cycle of debt.

Pros and cons of a debt consolidation loan for bad credit

Pros

- Save money with lower interest rates than you’re currently paying

- Can reduce the size — and number — of monthly payments

- Could improve your credit score if you can keep up with your new payments

Cons

- Hard to get low rates with bad credit

- May not qualify for a large enough loan to pay off all debts

- New hard inquiry can hurt your credit

Alternatives to consolidating debt with bad credit

Credit counseling or debt management plan

If you’ve fallen into debt, you could contact a nonprofit credit counseling agency that helps people negotiate with creditors and creates a debt management plan. Debt management plans can simplify your monthly debt payment, much like a consolidation loan does.

Credit counselors often are an affordable option relative to financing your debt, but make sure you find a credit counselor who meets your specific needs. They can also help you create a budget and teach money management skills.

Home equity loan

Sometimes you can get lower rates when you use your home as collateral. With a home equity loan or home equity line of credit (HELOC), you can use your home to finance your new loan — but watch out, because nonpayment can eventually lead to foreclosure.

Other secured loan

Using collateral like cars, bank accounts and other valuable items can help you qualify for lower rates. Secured loans will likely have better terms — but again, they come with the risk that the lender will take your asset if you stop making payments.

401(k) loan

Some companies let you borrow from your 401(k). The interest you pay goes back into your 401(k), but you can only borrow up to half of the vested amount or $50,000 (if the vested amount is higher). You might also have to pay the balance in full if you leave your job.

When banks compete, you win

You’d shop around for flights. Why not your loan? LendingTree makes it easy. Fill out one form and get lenders from the country’s largest network to compete for your business.

Tell us what you need

Take two minutes to tell us who you are and how much money you need. It’s free, simple and secure.

Shop your offers

Our users get 18 personal loan offers on average. Compare your offers side by side to get the best deal.

Get your money

Pick a lender and sign your loan paperwork. You could see money in your account in as soon as 24 hours.

Why trust our methodology?

Our writers and editors dig through the facts, contact lenders directly and even go through the application process ourselves if it helps better explain what you can expect. As a Certified Financial Education Instructor℠, I’m committed to breaking down complex financial details so people can make confident, informed decisions with their money.

Jessica’s experience in editing and financial education helps shape LendingTree articles that are clear, accurate and truly useful to readers. Her certification means our recommendations are built on a foundation of consumer-first financial knowledge — not just numbers.

What sets LendingTree content apart

Expert

Our personal loan writers and editors have 32 years of combined editorial experience and 28 years of combined personal finance experience.

Verified

100% of our content is reviewed by certified personal finance professionals and meets compliance and legal standards.

Trustworthy

We put your interests first. We’ll tell you about any loan drawbacks and be clear about when to consider alternatives.

Frequently asked questions

If you’re able to keep up with your loan payments, debt consolidation loans may actually improve your credit score. As you pay off your debt, you’ll show creditors that you can make payments on time. Over time, this can boost your credit score.

Different lenders have different credit score requirements. Some will require that you have a good credit score, while others will accept fair credit. The lower your credit score, the higher your APR will likely be.

Yes, you can get a debt consolidation loan with bad credit. However, you’ll likely pay high rates, and you may need to take out a secured loan or apply with a co-borrower. If you’re stuck with high rates, you can always refinance your personal loan down the road.

If you want to apply for a debt consolidation loan but have a lot of debt, getting approved may be difficult, but not impossible. For starters, check your credit score to see where you stand and work on cutting down on your debt. You can do this by using methods like the debt snowball method or the debt avalanche method.

Our methodology

LendingTree’s team of expert writers and editors reviewed more than 30 lenders and lending platforms — and shopped directly with 15 of them — to find the best debt consolidation loans for bad credit. To make our list, lenders must offer debt consolidation loans, advertise a minimum credit score of 580 or lower and cap their annual percentage rates (APRs) at 36% or lower.

According to our systematic rating and review process, the best personal loans for bad credit come from Upstart, Best Egg, Upgrade, Avant and OneMain Financial. LendingTree reviews and fact-checks our top lender picks on a monthly basis.

Accessibility. We look for lenders with fewer barriers to approval and award points for lower credit requirements, nationwide access, fast funding and simple applications.

Rates and terms. We prioritize lenders that offer low starting rates, minimal fees, flexible terms and APR discount opportunities.

Repayment experience. We choose lenders with strong reputations, convenient self-service tools, responsive support and borrower-friendly perks.