Citibank Personal Loan Review

Citibank pros and cons

Citibank personal loan requirements

| Citibank loans CAN be used for… | Citibank loans CANNOT be used for… |

|---|---|

|

|

If

How to get a personal loan with Citibank

How Citibank compares to other personal loan companies

| bank | LightStream | ||

|---|---|---|---|

| LendingTree’s rating | 3.4/5 | 3.9/5 | |

| Minimum credit score | |||

| APRs | (with autopay) | 7.99% – 24.99% | |

| Loan amounts | $2,500 – $40,000 | ||

| Repayment terms | months | months | 36 to 84 months |

| Origination fee | |||

| Funding timeline | Receive funds from as soon as the same day to within two business days | Receive funds in as little as 24 hours | Receive funds as soon as the next business day |

| Bottom line | bank might be the most competitive if you have good (not excellent) credit, as it has the lowest maximum APR. | accepts less-than-perfect credit, but it charges an origination fee. | LightStream has long loan terms that let you stretch out payments, but loans start at $2,500. |

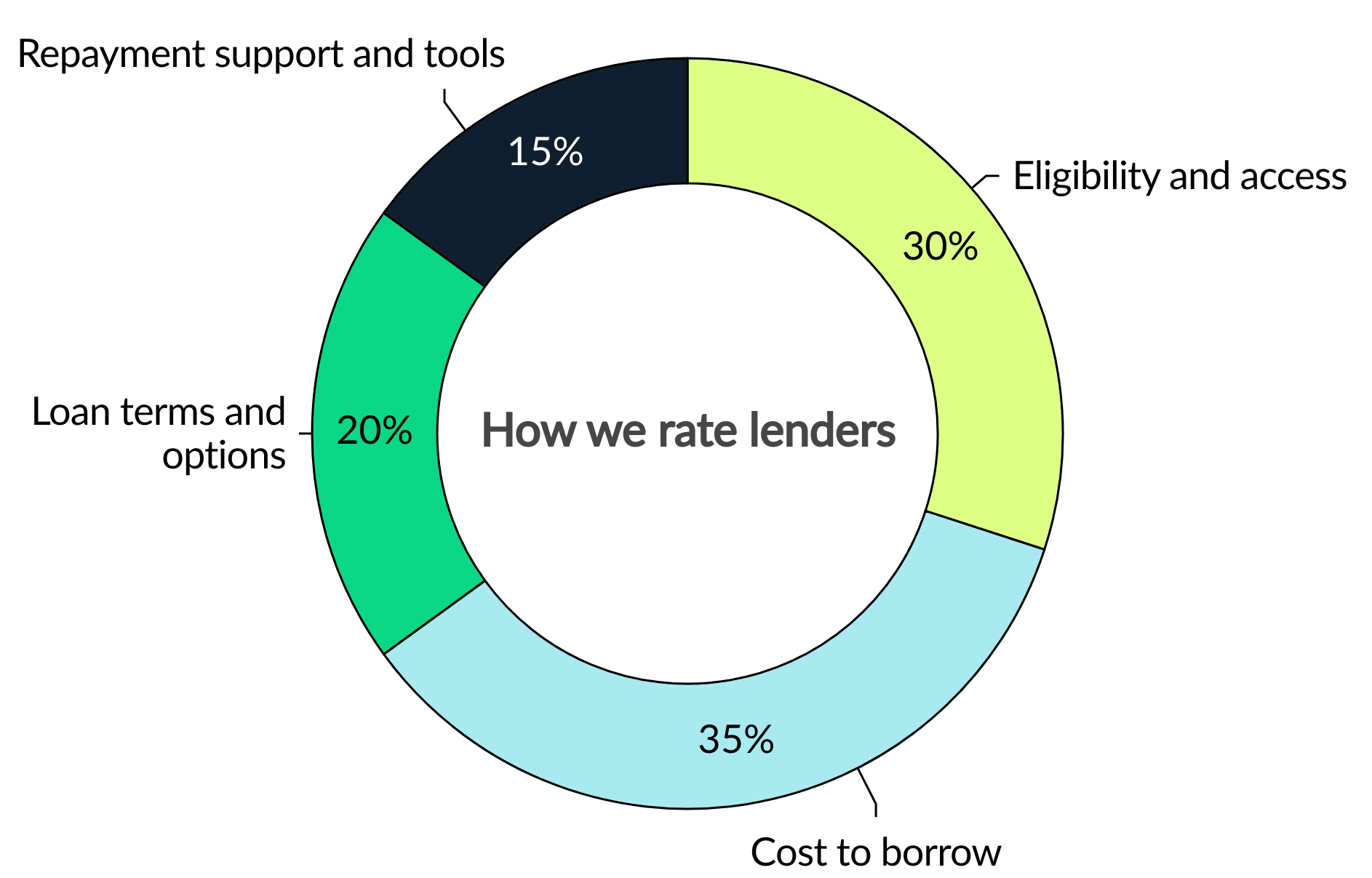

How we rated Citibank

We evaluate personal loan lenders on more than just interest rates. Our goal is to show how accessible, affordable, transparent and supportive each lender really is.

Our categories

Every lender is scored out of 5 stars, with 5 stars being the highest rating. LendingTree loan experts determine this score using dozens of underlying data points across four weighted categories covering the full borrowing journey.

We assess how easy it is for people to qualify and apply. This includes state availability, soft-credit prequalification, membership requirements, funding speed and whether borrowers with less-than-excellent credit can get a loan.

We evaluate how affordable the loans are based on minimum and maximum APRs, loan fees and rate discounts. Lenders with unclear or potentially predatory costs receive lower scores.

We consider repayment term flexibility, loan amount ranges and whether options like secured loans, joint loans or direct-to-creditor payments are offered — plus whether the lender clearly communicates these options.

We evaluate borrower experience after funding: customer service access, hardship or forbearance programs, payment flexibility and digital tools like mobile apps or credit monitoring.

Our process

We gather data directly from lenders through their websites, disclosures and direct communication with company representatives. Our editorial team verifies and updates information regularly. We value transparency and award less favorable scores when lenders obscure or omit details.

In some cases, our editors may apply a small adjustment (no more than 4% of the overall score) to account for factors not captured by the methodology. This could include J.D. Power customer satisfaction surveys, recent regulatory actions or features that stand out in ways our rubric doesn’t measure directly.

Our editorial team applies the same scoring model and standards to every lender. Lenders cannot pay to influence our ratings.